Why Europe, why now?

European deep tech and the techno-renaissance

Europe has always been a continent of inventors. From the printing press to the programmable computer, from electromagnetic induction to the World Wide Web, breakthroughs born on European soil have reshaped entire civilisations. And yet the continent has spent the better part of three decades watching others - principally America and China - capture the commercial value of those breakthroughs.

The popular narrative about Europe is often pushed as one of managed decline - a continent rich in heritage but poor in ambition, watching helplessly as Silicon Valley and Shenzhen build the future. It has become a kind of intellectual crutch: Europe invents, America scales, China manufactures.

That pattern now has a chance of breaking. A convergence of geopolitical pressure, maturing venture capital, and a new generation of science-rooted founders is creating the conditions for what I would fairly call a European techno-renaissance - ventures grounded in scientific and engineering breakthroughs rather than incremental improvements which play directly to Europe’s existing strengths in research, precision manufacturing, and industrial complexity. Across fusion labs in Munich, robotics corridors in Zurich, and AI workshops in Paris, a generation of founders are building the future of society

The question worth asking is no longer whether Europe can compete. The question is whether the institutions, investors, and founders on this continent can organise themselves quickly enough to capture the value from what they have already built.

Let’s explore how far we’ve come and why we are at an inflection point right now.

1) Europe as the historical engine of innovation: the continent that built the modern world

The sheer density of foundational technologies that originated in Europe is easy to forget precisely because they have become so embedded in daily life. Every foundational layer of the modern economy - energy, computation, communications, biology, transport - was either discovered or industrialised on this continent.

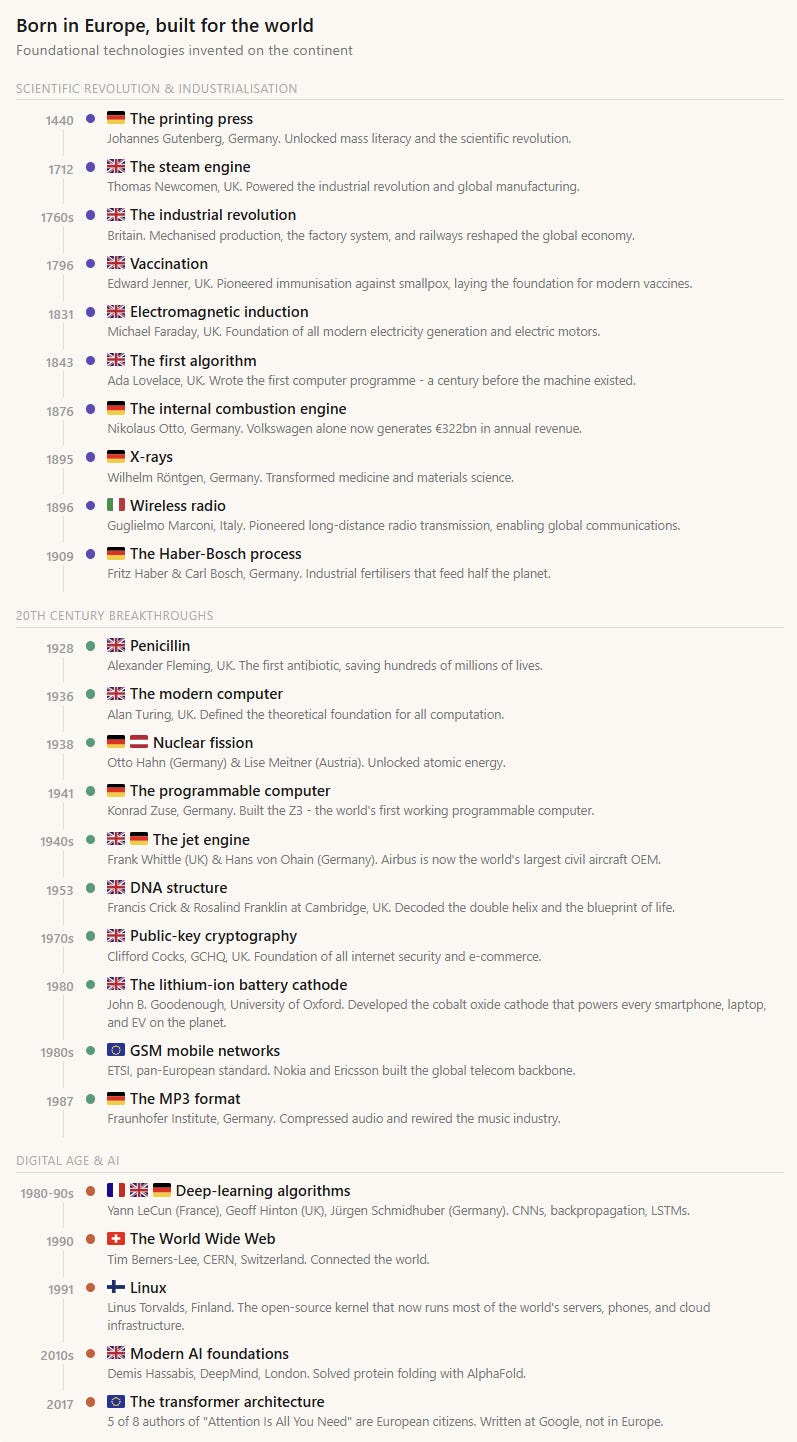

Ada Lovelace wrote the first algorithm in 1843. Alan Turing defined the theoretical model of the modern computer in 1936. Konrad Zuse built the first programmable machine in Berlin in 1941. The jet engine was co-invented in Britain and Germany in the 1940s, and Europe doubled down on aerospace to produce Airbus - now the world’s largest civil aircraft manufacturer and a technology magnet for more than 2,000 suppliers. German engineers industrialised the internal combustion engine. BASF turned the Haber-Bosch process into Europe’s chemical powerhouse, producing the fertilisers that feed roughly half the planet. ASML in the Netherlands is responsible for 100% of the extreme ultraviolet lithography systems required to produce the most advanced semiconductors on earth. Nokia and Ericsson built the backbone of global telecommunications. The GSM standard, designed by pan-European collaboration in the 1980s, became the dominant mobile protocol worldwide.

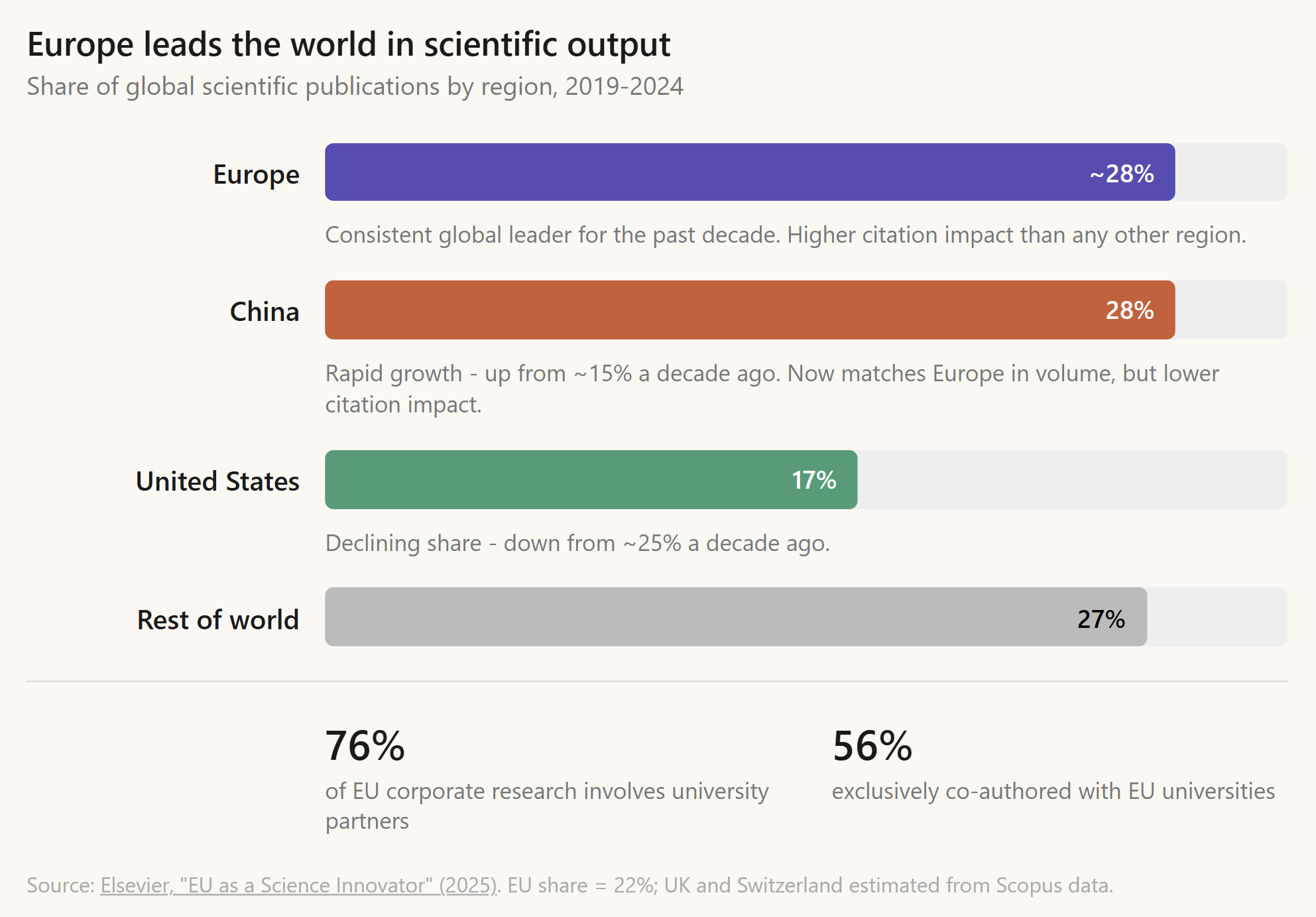

Europe - counting the EU, UK, and Switzerland - has consistently led the world in scientific output, holding roughly 28% of global publications over the past decade. 1 China has ramped up aggressively and now matches that figure, while America's share has declined to 17%. But volume is only part of the story: European research is cited more frequently than Chinese research, and the continent leads globally in life sciences, biotechnology, photonics, robotics, and space technology. ETH Zurich, Imperial College, the Max Planck Institutes, Cambridge, Oxford, EPFL - these are Tier 1 institutions that serve as the training grounds for a disproportionate share of the people running the most consequential technology labs on the planet.

The trouble for Europe is that scientific output and commercial capture are two different things…

2) Where it went wrong: How Europe lost decades of value creation

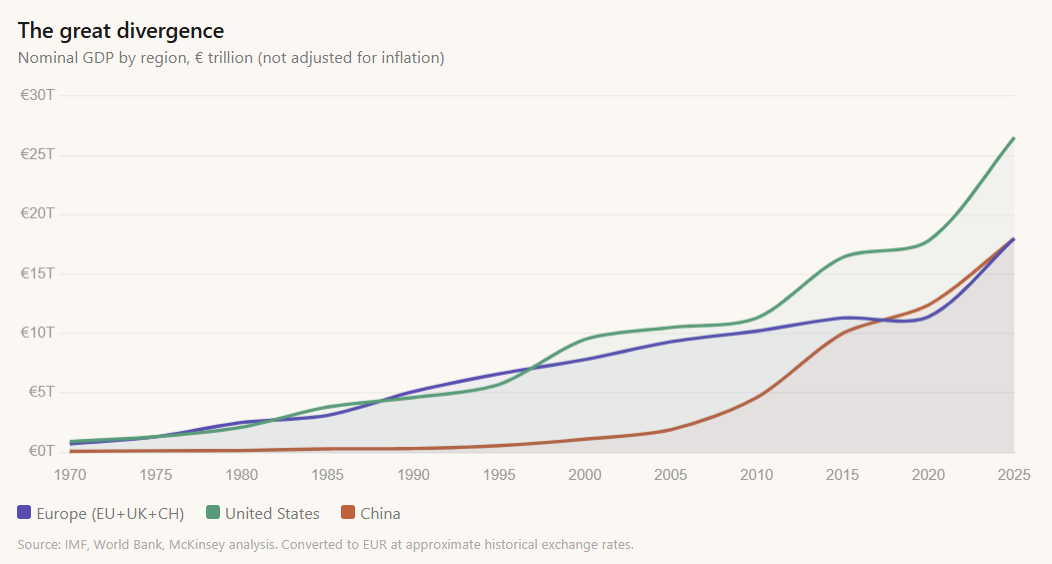

Europe led the world in industrial innovation through the 1970s and 1980s, and the economic results followed. But when the internet emerged in the 1990s, the continent's GDP growth trajectory began to diverge from America's - and has not converged since. China, meanwhile, went from a negligible share of global output to matching Europe's GDP in barely two decades, powered by manufacturing scale and, increasingly, technology investment.

Europe's GDP growth slowed from roughly 2-3% annually in the 1980s to approximately 1% after 2010. America sustained around 2.5-3% across the same period, driven by successive waves of technology-driven value creation in software, healthcare, and biotech. China grew at nearly 10% per year for most of that window.

There is, however, a flicker of momentum. Eurozone GDP accelerated from 0.4% in 2023 to 0.9% in 2024 and 1.4% in 2025 - modest by global standards, but the strongest trajectory since the post-pandemic rebound, driven by recovering consumption, easing interest rates, and rising investment. Europe's tech sector has surged to a combined value of nearly $4 trillion, a fourfold increase over the past decade. 2

Mario Draghi's 2024 competitiveness report lays out the structural causes that have led Europe to lag behind despite having all the ingredients to dominate at the global stage. The main causes are boiled down to:

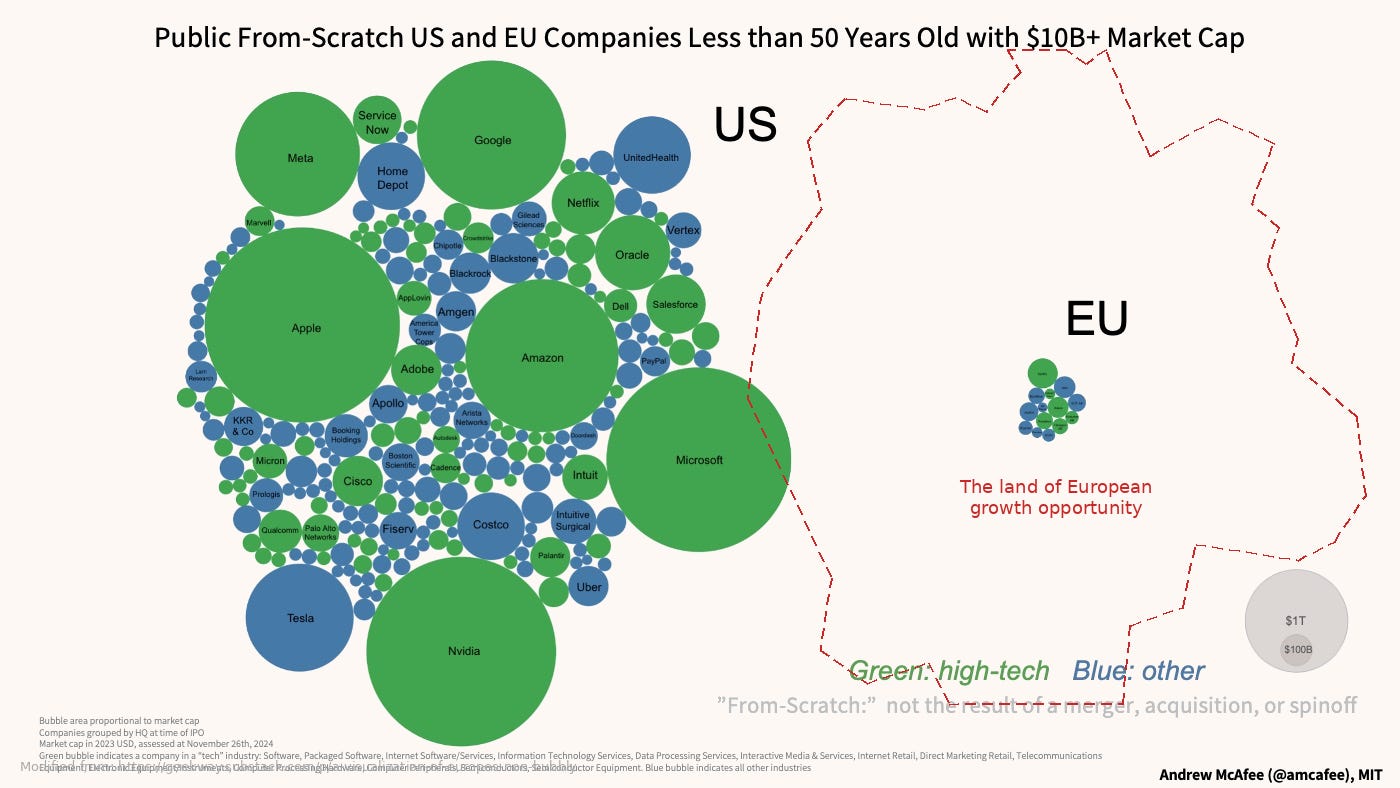

Fragmented markets and regulatory friction (i.e. we still need to build a single market !): The EU's 27 member states each carry their own regulations, tax regimes, and labour laws. The IMF recently estimated that intra-EU trade barriers create the equivalent of a 44% tariff on goods - three times the barrier between US states - and 110% for services. Scaling across Europe remains a legal labyrinth. The result is that no EU company with a market capitalisation above €100 billion has been created from scratch in the past fifty years. The United States has produced six companies currently valued above €1 trillion in that window.

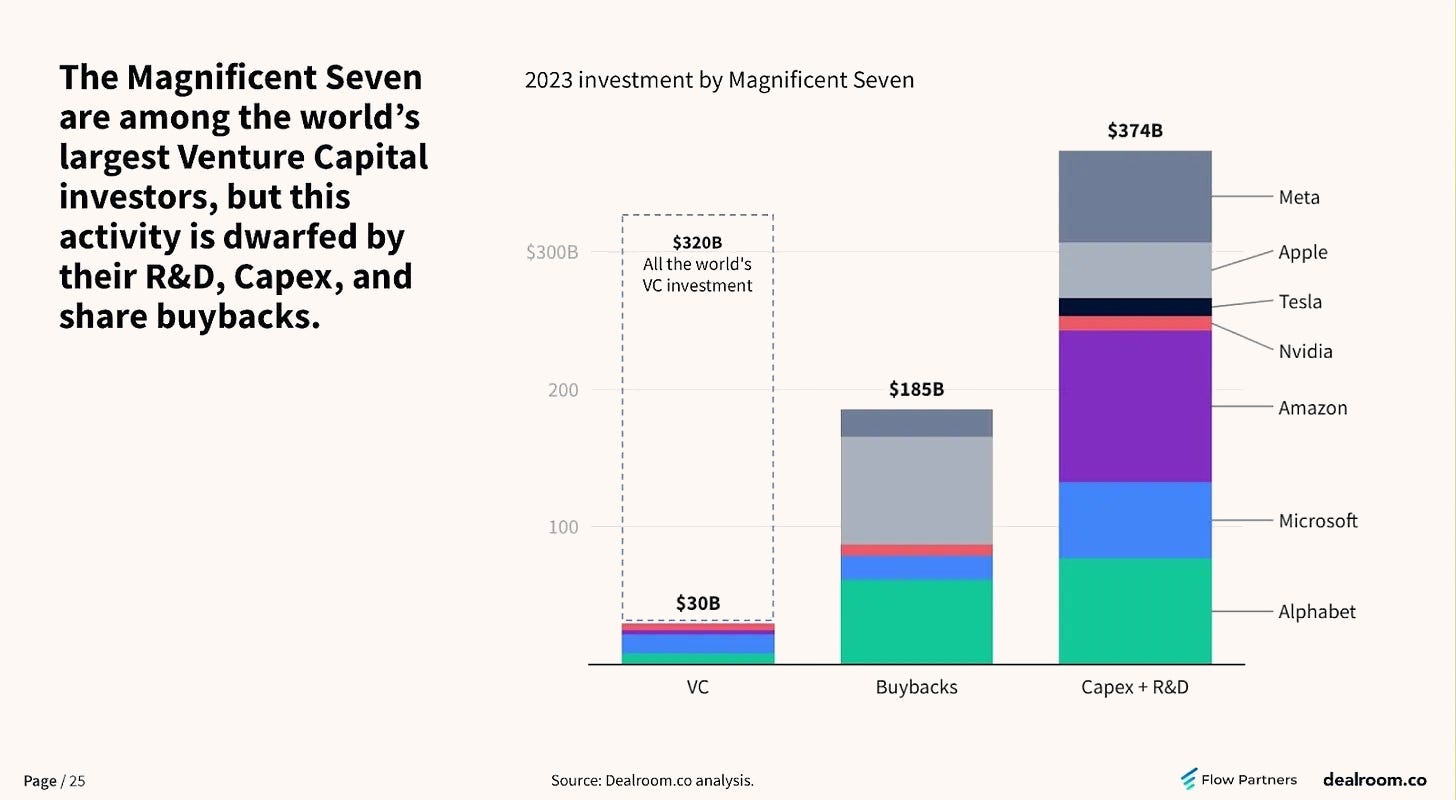

Europe's corporates are not spending enough on technology: Europe's large firms spend roughly 5 times less on technology R&D than their US counterparts. In 2023, the Magnificent Seven alone spent $374 billion on capex and R&D, more than the $320 billion in total venture capital deployed globally that same year. Venture capital, for all the attention it receives, is a rounding error next to corporate investment. The companies that shape the technological frontier are the ones that spend the most on building it - and Europe has no equivalent cohort. If the continent wants to lead in the industries of the next century, its corporates need to move from writing modest venture cheques to becoming the primary engine of technology investment.

The scale-up exodus: Between 2008 and 2021, close to 30% of European unicorns relocated their headquarters abroad, overwhelmingly to the United States. The playbook repeats itself: a founding team emerges from a European university, builds a working prototype, raises a seed round from local investors - and then, when the company reaches the stage where it needs $100 million or more, it discovers that the capital, the customer base, and the operating environment all point towards America. The result is a paradox where nearly a quarter of the world's unicorn founders are European by origin, yet only 6% of global unicorn value is captured in Europe.3 OpenAI, Stripe, Shopify, and Palantir were all founded or cofounded by Europeans, yet, they were all built in America.

The pattern holds across every wave. Take telecommunications: Europe built the global backbone through Nokia and Ericsson, then watched the platform layer - the layer where nearly all the value accrued - get captured by American and later Chinese firms. Or deep learning: European researchers pioneered the algorithms; the trillion-euro companies those algorithms spawned were built elsewhere. In each case, the science was European, the commercial returns were not.

3) The European techno-renaissance: the €1 trillion opportunity hiding in plain sight

The conditions that prevented Europe from capturing the commercial value of its own inventions for decades are now tangibly reversing.

As we’ve seen, Europe has historically been extremely good at foundational technologies, what we know as Deep Tech. Companies grounded in scientific and engineering breakthroughs that require intensive R&D and typically involve hardware - play to Europe’s latent advantages. The continent’s 5,000-plus universities, its deep industrial base in precision manufacturing, and its cultural affinity for rigorous engineering all translate well when the challenge is not building another SaaS product but mastering fusion physics, designing antibody-drug conjugates, or training a humanoid robot to navigate a factory floor.

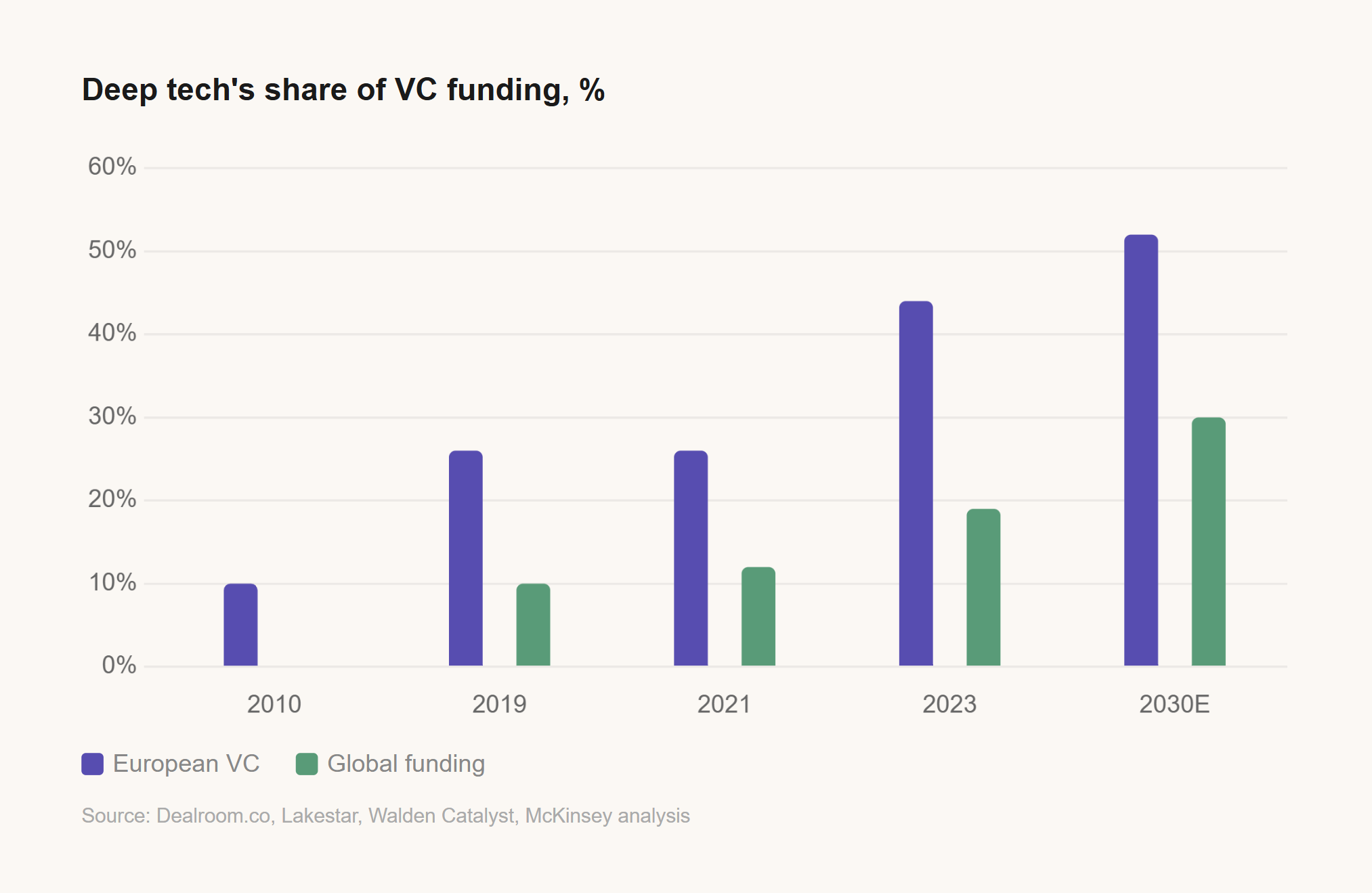

What are we seeing changing? on the funding front, between 2019 and 2023, Europe’s share of global deep-tech investment nearly doubled, rising from 10% to 19%. Within Europe itself, deep tech now commands approximately 44% of all tech investment - up from 26% in 2019. Venture capital allocated to European deep-tech ventures has grown fivefold over the past decade.

Why does this matter? Because the centre of gravity in technology investment is shifting toward building the new foundations of the economy - and deep tech is becoming an investable category in its own right, pulling more capital in with each cycle. The returns justify the attention. Deep-tech funds have delivered an average net IRR of 16-17% after all fees since 2003, compared with 10% for traditional technology funds.4 European deep-tech unicorns reach $1 billion valuations 28 months faster than their regular-tech counterparts, hold nine times more patents, and generate 12% higher money-over-money returns for investors.

This is the structural advantage of the continent: The high barriers to entry in deep tech - scientific complexity, capital efficiency, and the technical literacy demanded of both founders and investors - create the kind of defensible positions that matter most when building foundational technology.

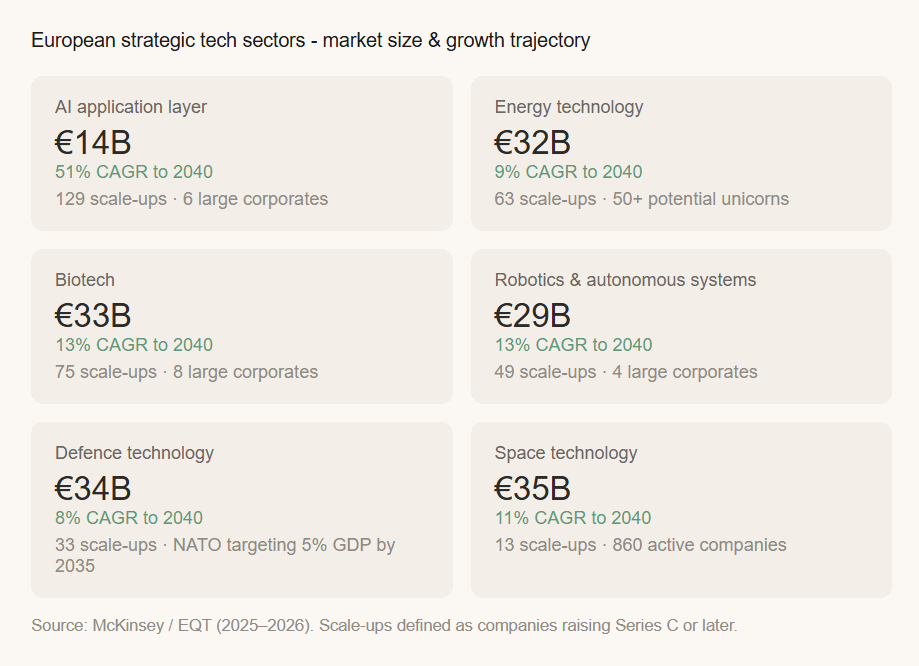

What we are seeing across Europe is the emergence of companies and hubs that are already world-leading, and on their way to becoming the key needle-movers in generating €1 trillion in new enterprise value across the continent within this decade. A few stand out:

AI application layer: Europe has a thriving ecosystem of applied AI companies, with several valued at €5-10 billion. Mistral AI raised a $2 billion Series C in September 2025, led by Dutch semiconductor champion ASML. Germany's Parloa raised €300 million at a €2.6 billion valuation in early 2026 for AI customer service agents. Equity funding for European enterprise AI startups more than doubled between H1 2024 and H2 2025, reaching €5.2 billion in a single half-year.

Energy and fusion: Europe's position in next-generation energy is less a sudden surge than the product of decades of accumulated expertise. The ITER megaproject and CERN have created a deep supply chain of precision manufacturers and a generation of physicists with practical intuition that cannot be replicated overnight. Munich-based Proxima Fusion signed a €2 billion programme with the State of Bavaria, RWE, and the Max Planck Institute to develop Europe's first commercial fusion power plant. Global fusion investment surged nearly 500% to €3.3 billion in 2025.

Biology and drug discovery: AI is collapsing timescales in biological research. Basecamp Research and partners unveiled foundation models trained on 10 billion previously unknown genes from over a million species - the first AI system capable of designing potential medicines across approaches from small molecules to gene therapies. AI-powered biotech funding in Europe trebled from €426 million in 2024 to €1.4 billion in 2025.

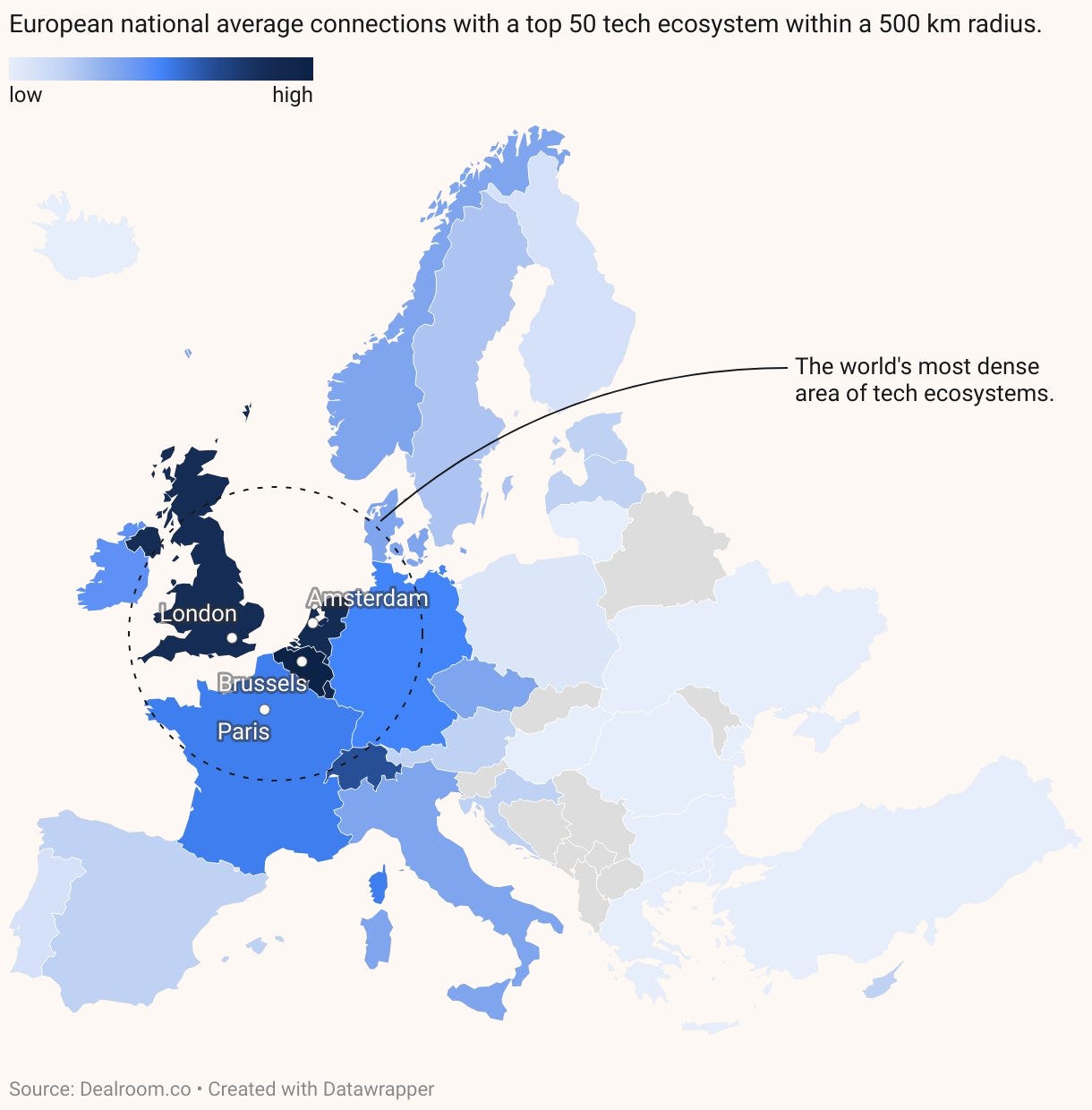

Robotics and physical AI: European investment in robotics startups surpassed €1.6 billion in 2025, more than doubling the prior year. The continent’s strength lies on the software and intelligence layer with the ETH-EPFL corridor in Switzerland emerging as a world-class robotics cluster. Think about the fact that only 30% of warehouses in Europe are automated - this alone is a gigantic market opportunity.

Defence and space. NATO members are now targeting 5% of GDP on defence spending by 2035, up from 2% before Russia's invasion of Ukraine - a 61% increase in Europe since 2020 that amounts to over €150 billion in additional annual spending, comparable in scale to the inflation-adjusted Marshall Plan. The dual-use model, where technologies scale commercially while also serving defence markets, is gaining traction rapidly - and for good reason: it lowers development costs, broadens the customer base, and makes the economics work for both investors and governments.

What makes this cycle different from prior European innovation waves is the convergence of three structural tailwinds.

First, the technologies in play are inherently suited to Europe's capabilities: Take fusion, for instance. It requires mastery of complex systems integration - high-temperature superconducting tapes, precision manufacturing of reactor components, and computational modelling at extreme scales. The US excels at software-speed venture capital; China dominates mass-volume replication. But fusion - and robotics, and advanced biologics - demands a middle-zone capability: high-complexity precision manufacturing where the winner is not the one with the fastest capital, but the one with the best integration of complex systems. That is Europe's historical sweet spot.

Second, the funding architecture is maturing: European VCs now outperform their North American peers on 10 and 15-year IRR horizons, according to Invest Europe and Cambridge Associates data. Sweden leads Europe in channelling pension capital into deep tech, with 65% of all startup funding directed to deep-tech companies. France's La Mission French Tech programme helped the country increase its unicorn count from 7 in 2015 to 42 in 2024 - one of the fastest growth rates on the continent. Total capital invested in European startups in 2025 reached its highest level since the boom years of 2021-22, and the sector's combined public and private value now stands at nearly €4 trillion.

Third, geopolitical necessity is concentrating efforts: The sovereignty imperative - driven by the war in Ukraine, supply chain vulnerabilities in critical minerals, historical dependence on American technology infrastructure, and the current unpredictability of US policy - has made it a strategic priority. Defence and Resilience spending commitments are accelerating across the continent. Europe's depth in supply chains, scientific talent, and precision engineering cannot be replicated overnight - and the geopolitical order is now forcing the continent to treat that depth as a strategic asset rather than a background advantage.

4) Time to change the narrative

There is one final ingredient for Europe to thrive that no policy paper or venture fund can supply on its own. It is the simplest and hardest thing to change: the story Europe tells about itself.

Walk into any European tech conference and you will hear the same refrain: "We're not Silicon Valley." We don't need to be. Accepting a narrative of permanent inferiority does not build competitiveness. Rather, it creates a self-fulfilling prophecy.

Alongside risk appetite, the single greatest advantage Silicon Valley holds over Europe is not capital density, nor university output. It is storytelling. The ability to take an idea - sometimes half-formed - and tell it in a way that makes it feel inevitable. Once a narrative takes hold, people rally behind it, capital follows, and the story becomes self-fulfilling. Europe has no equivalent engine. The continent has people building extraordinary things in labs in Zurich, factories in Munich, research centres in Cambridge and Delft. But these stories are undersold, underhyped, and systematically undervalued by a media and investor class that still takes its cues from San Francisco.

France has begun to show what is possible when a government decides to project confidence rather than apologise for ambition. President Macron's "France is Wild" campaign struck a nerve precisely because it broke with the European tradition of institutional modesty. Conviction and storytelling move the needle far more than endless policy papers and reports ever will.

Europe’s investment culture has been historically risk-averse, and the consequences are massive, with around 60% of Europe’s top tech acquisitions made by non-European buyers. Institutions and corporates are too cautious to bet on their own ecosystem.

But the culture is shifting - and fast. Defence tech, a sector that European VCs considered effectively off-limits before 2020, now accounts for 6.2% of all European venture funding; at least 30 ESG-linked funds have added aerospace and defence holdings.

Founders are changing too: Synthesia rejected a $3 billion acquisition from Adobe; ElevenLabs and Mistral turned down buyouts to scale independently; European startups are increasingly retaining their headquarters on the continent rather than decamping to Silicon Valley. This shift needs to accelerate. In a world where technological capacity increasingly underpins sovereign influence, risk aversion is itself the riskiest posture of all !

This culture does not change from the top down. It changes from the bottom - where individuals decide to act differently. If you allocate capital, make European technology a core position. If you run a corporation, co-develop with the startups in your own ecosystem. If you are a founder, build from here with global ambition and say so publicly. If you work in procurement, give European technology companies a real shot at the contract. If you are a researcher, talk to a tech transfer office this quarter. And if none of these apply, do the simplest thing: share the European technology stories that cross your feed. Waiting for someone else to go first is precisely the habit that needs breaking.

Europe does not need permission to compete - we need to start telling our story with the same conviction we have in our science. We have all the necessary ingredients to become once again a powerhouse, now is the time to cook.

And remember, don’t be shy, don’t be apologetic, don’t mask your ambition - the world needs to hear the great things we are building.